Difference Between Cheque and Demand Draft: Which Payment Method Is Safer and Why

At some point, almost everyone has to choose between issuing a cheque or getting a demand draft. It looks like a small decision, but it can affect whether a payment is accepted immediately or delayed without warning. Cheques and demand drafts both move money, but they do it in very different ways. Understanding the difference between a cheque and a demand draft can save a lot of time.

What is a Cheque?

A cheque is a written and signed instruction given by an account holder to their bank, asking it to pay a specific amount to a person or organisation. It works as a paper-based alternative to cash, which allows money to be transferred safely without physically handling currency.

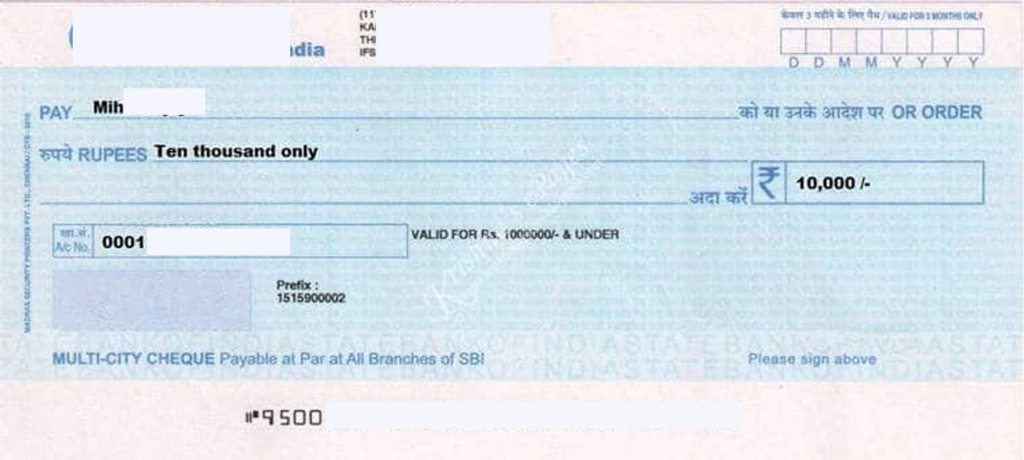

Cheque Example

Key Components of a Cheque

- Drawer: The account holder who writes and signs the cheque.

- Drawee: The bank on which the cheque is issued.

- Payee: The individual or organisation receiving the payment.

- Amount: The exact sum to be paid, written in words and figures.

- Date: Determines the validity period of the cheque.

- Signature: Confirms that the drawer has authorised the payment.

What are the Advantages of a Cheque?

A cheque may look old-fashioned, but in many real situations it offers flexibility and control that instant payments do not.

- Using a cheque feels safer than carrying large amounts of cash for rent, fees, or business payments.

- Every cheque leaves a paper trail, which makes tracking expenses, accounts, and disputes much easier.

- If something goes wrong, you can ask the bank to stop the payment before the cheque is cleared.

- Cheques usually do not involve extra charges, making them a cost effective option for regular payments.

- You can post-date a cheque to plan future payments, and it works even without internet access.

- A cleared cheque and bank statement together act as solid proof of payment.

What are the Disadvantages of a Cheque?

Cheques may feel safe, but they are not always the most reliable way to move money.

- Cheques take time to clear, so the money does not reach the other person immediately.

- There is always a risk of the cheque bouncing if the account does not have enough balance.

- Cheques can be misused or forged since they carry sensitive banking details.

- Handling cheques means paperwork, safe storage, and bank visits, which can be inconvenient.

- Many people and businesses no longer accept cheques due to faster digital options.

Types of Cheques You Should Know About

Cheques are issued by account holders and are commonly classified based on how they are paid and their validity.

| Type of Cheque | Purpose |

| Bearer cheque | Can be encashed by anyone who presents it at the bank, usually without identification |

| Order cheque | Payable only to the person or organisation named on the cheque |

| Crossed cheque | Must be deposited into a bank account and cannot be encashed directly |

| Account payee cheque | Can be credited only to the payee’s bank account, making it safer |

| Self cheque | Used by the account holder to withdraw cash from their own account |

| Post-dated cheque | Has a future date and can be processed only on or after that date |

| Stale cheque | Becomes invalid if not presented within the validity period, usually three months |

| Mutilated cheque | A damaged or torn cheque may be rejected unless verified by the bank |

What is a Demand Draft (DD)?

A Demand Draft, commonly known as DD, is a prepaid banking instrument issued by a bank to transfer a fixed amount of money to a specific payee.

A DD guarantees payment and does not carry the risk of bouncing like a cheque. This is because the funds are collected in advance by the bank.

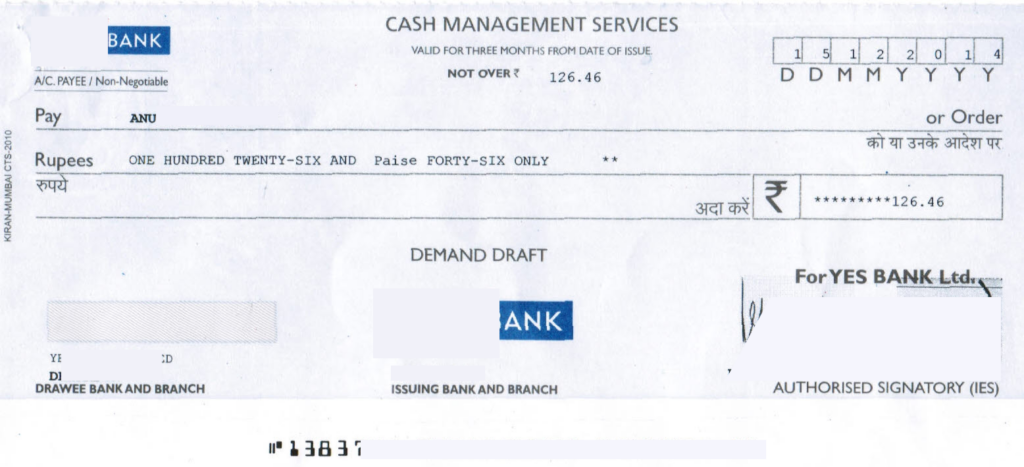

Draft Example

Key Components of a Demand Draft

- Issuing bank and branch details: Shows which bank and branch have issued the draft and are guaranteeing the funds.

- Date of issue: Indicates when the demand draft was created and becomes valid.

- Payee’s name: The person or organisation authorised to receive the payment.

- Amount payable: The fixed sum written in both figures and words, with the written amount taking priority in case of differences.

- Serial number or unique ID: Used for tracking, verification, and record keeping.

- Authorised bank signatures: Confirms that the draft has been officially issued and guaranteed by the bank.

- Security features: May include watermarks or other safeguards to prevent fraud.

- Payable bank branch: Specifies the branch where the draft can be presented for payment.

- Applicant’s details: Records the name of the person or entity that requested and paid for the demand draft.

What are the Advantages of a Demand Draft?

Unlike cheques, demand drafts remove the risk of payment failure from the equation.

Let us explore the advantages of using a demand draft!

- Guaranteed payment because the bank collects the money in advance, so there is no risk of the DD bouncing due to insufficient funds.

- Higher security as the DD is issued in the name of a specific payee and does not depend on the payer’s signature, which reduces misuse and fraud.

- Widely accepted by colleges, government departments, courts, and large organisations that need assured payments.

- Suitable for large amounts since there is usually no upper limit, making it useful for property purchases, vehicle payments, or major fees.

- No bank account required, as even non-account holders can get a DD by paying cash, subject to regulatory limits.

Disadvantages of Demand Draft

Demand drafts involve bank charges, take longer to process, and are difficult to cancel once issued.

- An extra cost is involved because banks charge issuance fees, which can feel unnecessary for small or frequent payments. This is usually a small fixed fee of around ₹25 to ₹40 for lower amounts and a per-thousand charge for higher values, with GST applied.

- Less convenient since it often requires visiting a bank branch and handling a physical document.

- Slower processing as DDs take time to be issued, delivered, and cleared, unlike instant digital transfers.

- Hard to cancel or refund once issued, especially if the DD has already been handed over to the payee.

- Risk of loss or damage because a DD is a physical paper instrument that can be misplaced or damaged

Types of Demand Drafts

Bank drafts, also called demand drafts, are prepaid instruments issued by banks that guarantee payment.

| Type of Demand Draft | Purpose |

| Sight demand draft | Payable immediately when presented, after basic verification |

| Time demand draft | Payable after a specified period or on a future date |

| Banker’s cheque or pay order | Similar to a demand draft, mainly used for local or same-city payments |

| Money order | Used to transfer a fixed amount from one place to another on behalf of a customer |

What is the Difference Between a Cheque and a Demand Draft?

The main difference between a cheque and a demand draft is who takes responsibility for the payment.

A cheque is issued by an account holder and depends on their bank balance, while a demand draft is issued and guaranteed by the bank after collecting the money in advance.

Cheque vs. Demand Draft: When to Use Which Payment Method

| Feature | Cheque | Demand Draft |

| Issued by | Account holder | Bank |

| Funds requirement | Balance is needed at clearance | Prepaid upfront |

| Risk of bounce | Possible if insufficient funds | None, guaranteed payment |

| Cost | Usually free | Bank fee applies |

| Cancellability | Yes | Difficult once issued |

| Security level | Lower risk if lost or misused | Higher, bank-backed |

Cheque or Demand Draft- Which One Should You Use?

Cheques are simple and flexible, making them suitable for everyday payments. But they carry the risk of failure if funds are not available.

Demand drafts are safer because the bank guarantees the payment, which is why they are preferred for high-value or official transactions where certainty matters.

Many government schemes require secure and verified payment methods through banks. If you want to understand eligibility, benefits, and payment processes, read our complete guide on the Ladli Behna Yojana and how beneficiaries receive financial support.

Whether you prefer the flexibility of cheques or the security of a demand draft, everything starts with a reliable savings account. A zero balance savings account lets you issue cheques, request demand drafts, and manage payments without worrying about minimum balance penalties.

Disclaimer- The rankings and figures in this article have been compiled from multiple verified reports, credible sources, and public financial data available as of 2026.

All values are approximate and may vary with newer updates, revisions, or changes in official records.

Cheque vs Demand Draft – FAQs

A Demand Draft is issued by a bank after funds are paid in advance, so payment is guaranteed. A cheque is issued by an account holder and can bounce if there are insufficient funds.

A cheque depends on the drawer’s bank balance and signature, while a draft is backed by the issuing bank itself. This makes a draft more secure and reliable than a cheque.

Yes, a Demand Draft can be obtained directly from a bank by paying cash or debiting an account. A cheque is not mandatory to issue a DD.

A draft is better because the bank guarantees payment, eliminating the risk of dishonour. It is widely accepted for high-value or official payments.

Yes, a Demand Draft is considered safer. This is because the money is already with the bank before issuance. This removes the risk of insufficient funds and reduces fraud.

Demand Drafts offer guaranteed payment, higher security, and faster acceptance for formal transactions. They are preferred for fees, property deals, and payments to institutions.